Abstract:Equiti review 2026: WikiFX score 5.06/10, CySEC and Seychelles licenses, CNMV warning, withdrawal complaints, clone alerts, and the Mediatrix lawsuit context.

Equiti is one of the more visible broker brands in the MENA market, but visibility alone does not settle the question of trust. A proper Equiti review has to start with the basics: its license structure, its WikiFX rating, the products it offers, the complaint pattern attached to the brand, and the external warning signals that have followed it in different jurisdictions.

On paper, Equiti has more structure than many offshore-only brokers. It also has enough negative signals to make a simple, one-sided conclusion inaccurate.

Contents

ContentsEquitis Basic Profile

The broker materials show Equiti as a multi-asset broker founded in 2008, registered in Seychelles, and offering access to FX pairs, commodities, digital currencies, shares, ETFs, and indices. It supports MT4 and MT5, provides a 90-day demo account with $10,000 virtual funds, and advertises leverage of up to 1:2000. The Standard account is shown with no minimum deposit and an average spread of 1.4 pips, while the Premier account starts from $100 and adds commission-based pricing. Customer support is listed as 24/6 live chat.

That is a commercially attractive profile. The problem is not the lack of products or platforms. The problem is whether the brokers regulatory structure and complaint history support the same level of confidence as its market presentation.

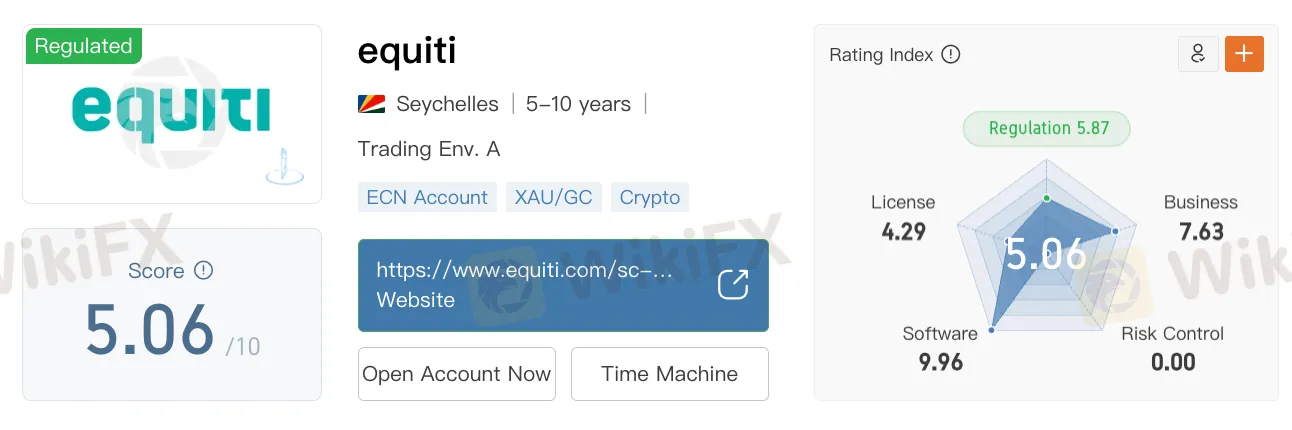

Equiti Rating on WikiFX

On WikiFX, Equiti currently holds a score of 5.06/10.

The page shows a rating breakdown of:

- Regulation: 5.87

- License: 4.29

- Business: 7.63

- Software: 9.96

- Risk Control: 0.00

The same page also indicates that the score has been reduced because of a high number of complaints. That detail matters. A mid-range score is not the same as a clean profile, especially when the weakest area is risk control, which stands at 0.00.

The full broker page is here:

https://www.wikifx.com/en/dealer/9641202830.html

Equiti License Structure

Equitis regulatory profile is one of the strongest reasons it remains relevant in the market. At the same time, it is also one of the main reasons the brand needs to be read carefully.

According to the broker page, Equiti holds two licenses:

- a CySEC Cyprus Forex Execution License

- a Seychelles FSA offshore derivatives license

This is not the profile of a no-license broker. The CySEC authorization gives Equiti a regulated foundation under a more established retail forex framework. The Seychelles license, however, is still an offshore authorization and should be understood as such. That means the Equiti license picture is mixed rather than uniformly strong.

In practical terms, the presence of a Cyprus license is a positive factor. The offshore Seychelles layer is less reassuring. That difference is important for any accurate تقييم Equiti or ترخيص Equiti analysis, because regulated does not always mean equally regulated across every entity under the brand.

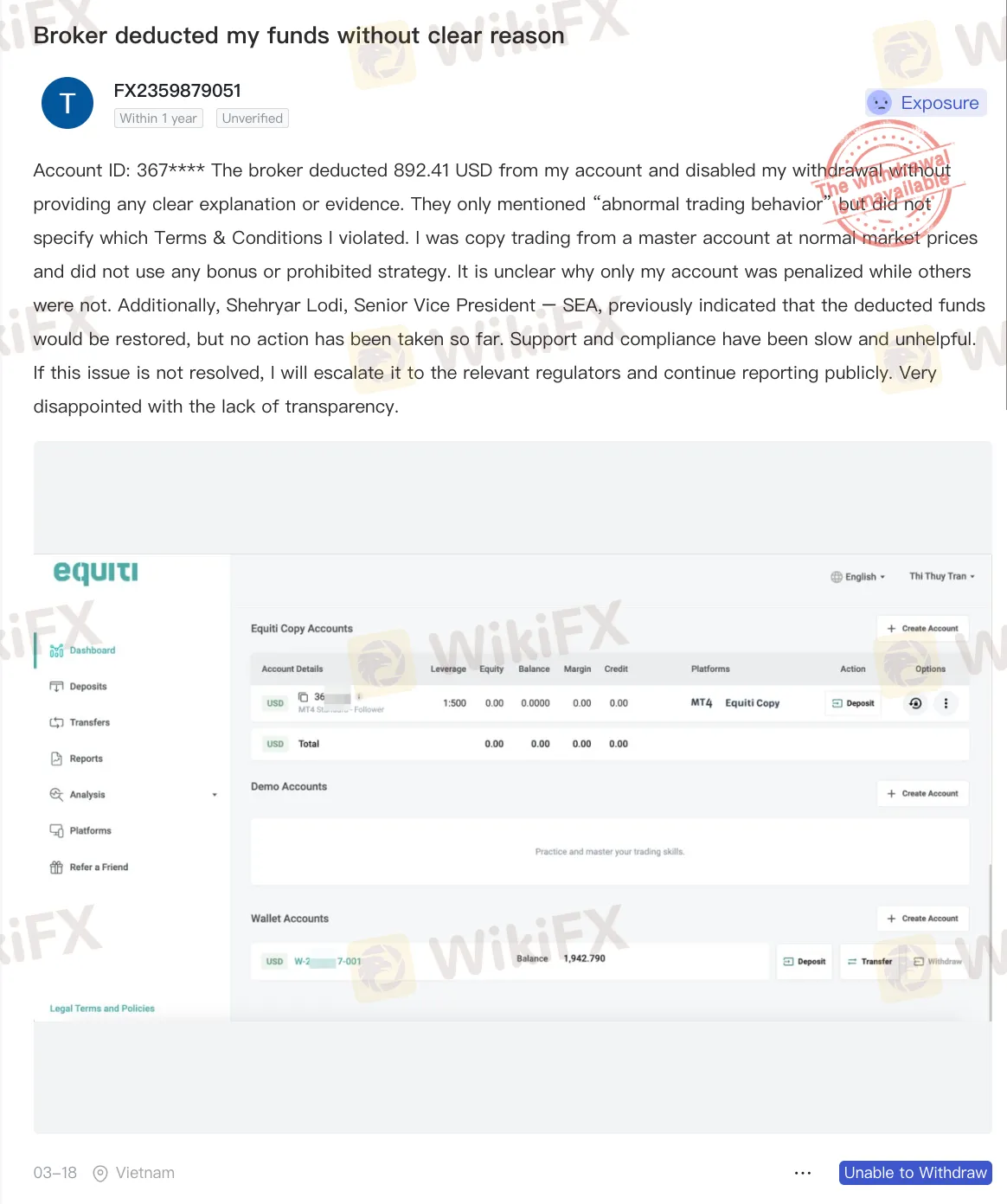

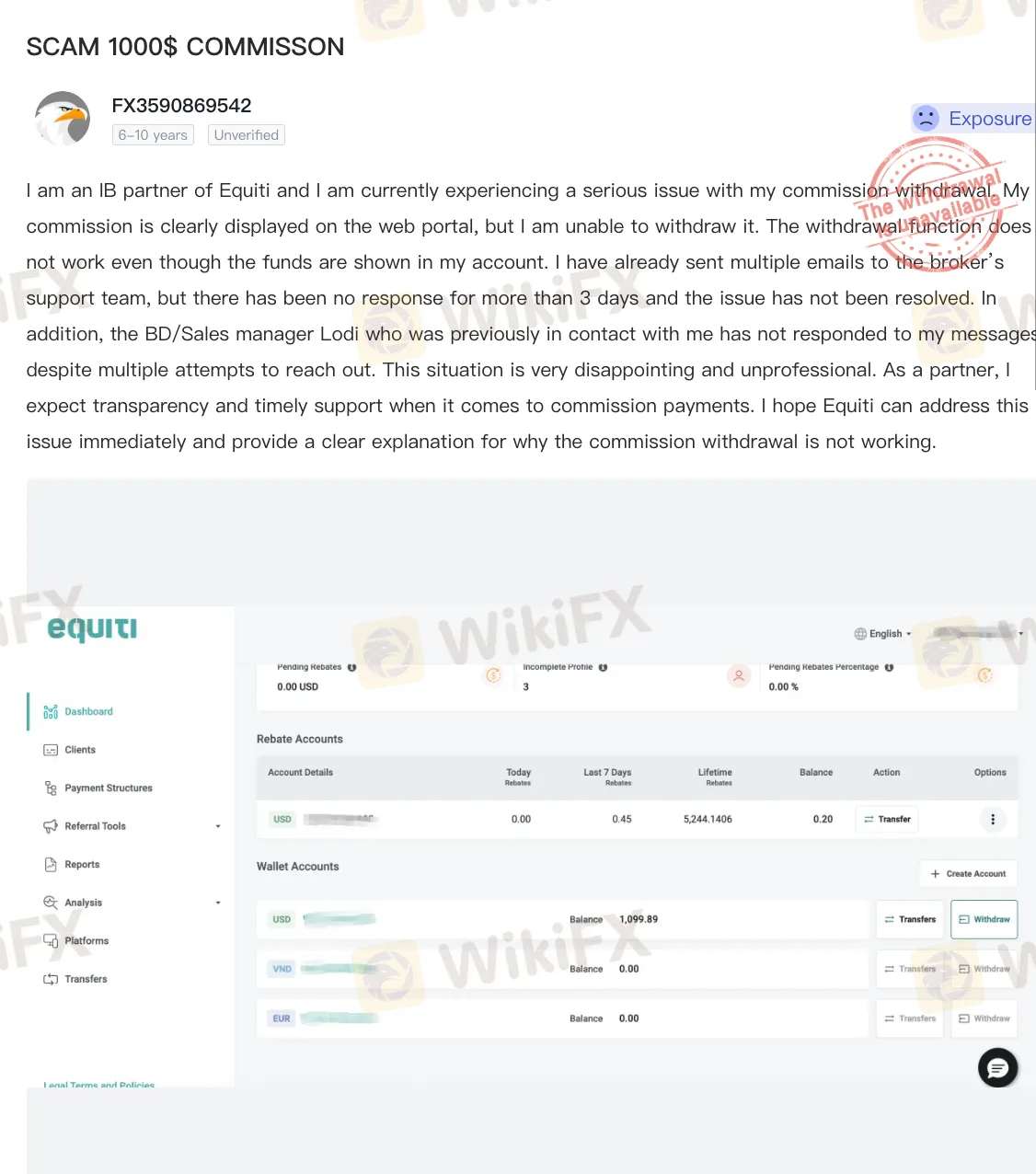

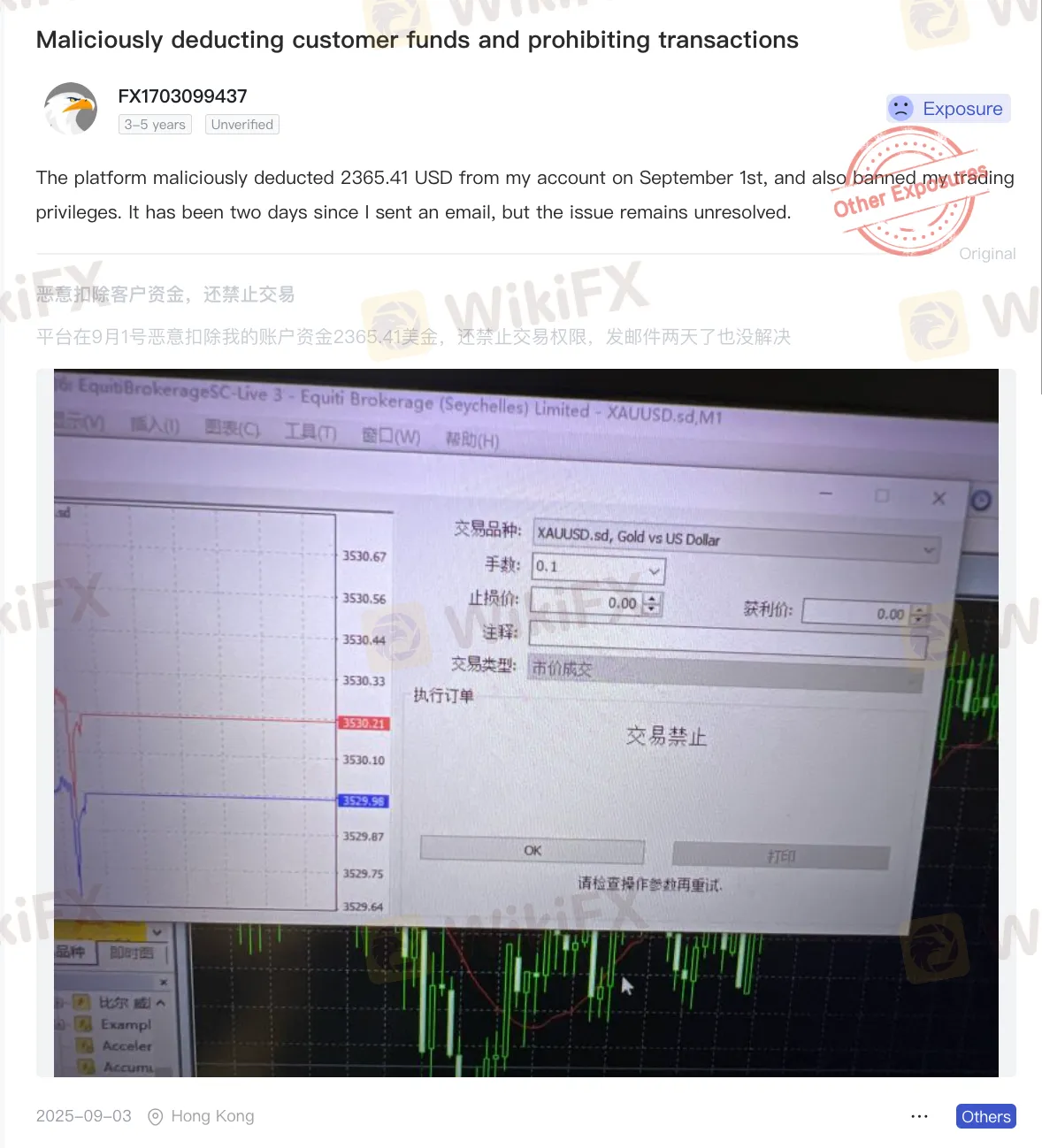

Complaints Focus on Deductions, Withdrawals, and Restrictions

The complaint section is one of the clearest weak points in Equitis profile.

The overall pattern is straightforward: several users claim that funds were deducted, withdrawal functions became unavailable, commissions could not be accessed, or accounts were restricted without a clear explanation. These are not minor service complaints. They go directly to account access and money movement.

One complaint states that $892.41 was deducted from the account and the withdrawal function was disabled, while the broker referred only to abnormal trading behavior without clearly identifying the rule allegedly broken.

Another complaint, filed by an IB partner, says that more than $1,000 in commission appeared in the portal but could not be withdrawn, with support and internal contacts failing to provide a timely resolution.

A third complaint says $2,365.41 was deducted and trading privileges were blocked.

A fourth alleges that after a long period of trading, the broker suddenly deducted both principal and profits, later claiming system abuse.

No individual complaint should be treated as a final ruling by itself. But when complaints repeatedly point to deductions, blocked withdrawals, disabled functions, and unclear explanations, the pattern becomes hard to ignore. For any broker review, that is a material factor.

CNMV Warning

The Equiti name has also appeared in warning contexts involving Spains CNMV.

Here, the concern is not simply brand confusion. The warning record is treated as indicating that the Equiti-linked operation in question was not authorised to provide investment services. That matters because it places the Equiti name inside a formal regulatory warning framework, not just inside general market criticism.

For a broker that already carries complaint pressure, a CNMV warning adds another layer of caution. It does not automatically cancel out the brokers other licenses, but it does make the overall risk picture more complicated.

Clone Warnings Around the Equiti Brand

A separate issue is the volume of imitation activity around the Equiti name.

In March 2024, the UAE SCA warned investors about MRL Investments Ltd, an unlicensed firm using highly similar domains such as equiiti.com and equiity.com to imitate the real Equiti brand. The regulator made clear that the scam operation had no connection with the legitimate Equiti entity.

The UK FCA also issued clone-related warnings involving entities trading on the Equiti name or closely related brand formats. In these cases, the core problem was impersonation: illegal platforms trying to benefit from the reputation of a regulated broker.

This does not mean the regulated Equiti entity itself was the clone. It means the brand has become a target for cloning, and that raises the operational risk for traders who do not verify the exact domain and entity before opening an account.

Involved in a Forex Fraud Lawsuit

Equiti has also been drawn into litigation connected to the Mediatrix Capital / Blue Isle forex fraud case.

This point does not need to be overstated. The existence of litigation is not the same as a final ruling of liability. Still, the fact that Equiti was pulled into proceedings tied to a major forex fraud case remains relevant from a reputational and legal-risk perspective. It is not the central issue in the brokers current profile, but it is part of the broader risk background and should not be omitted from any serious مراجعة Equiti.

Final Assessment

Equiti is not a broker that can be judged from one dimension alone.

It has a CySEC-regulated entity, an offshore Seychelles license, a broad product range, MT4/MT5 support, and a visible market presence. These are meaningful strengths. At the same time, its 5.06/10 score, 0.00 risk-control rating, complaint pattern around deductions and withdrawal restrictions, CNMV warning context, repeated clone activity around the brand, and legal exposure linked to the Mediatrix matter all remain relevant factors.

The more balanced conclusion is that Equiti has a stronger regulatory and operational foundation than many weaker offshore brokers, but its profile is not without pressure points. A proper review should consider both the licensed structure and the complaint record, while also distinguishing between the brands regulated entities and the repeated misuse of its name in clone-related cases.

Before opening any account, attention should be paid to the exact entity, the exact domain, the applicable license, and the most recent complaint history.