Global Broker Regulation Inquiry App

About WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

اردو

Gold Surpasses U.S. Treasuries as the World's Top Central Bank Reserve Asset

Abstract:Market OverviewA historic shift in global reserve management is underway. According to the European Central Bank (ECB), gold accounted for 27% of global central bank reserve assets by the end of 2025,

Market Overview

A historic shift in global reserve management is underway. According to the European Central Bank (ECB), gold accounted for 27% of global central bank reserve assets by the end of 2025, surpassing U.S. Treasuries at 22% for the first time. This marks a major milestone in the global reserve landscape and highlights growing central bank demand for gold amid rising geopolitical uncertainty.

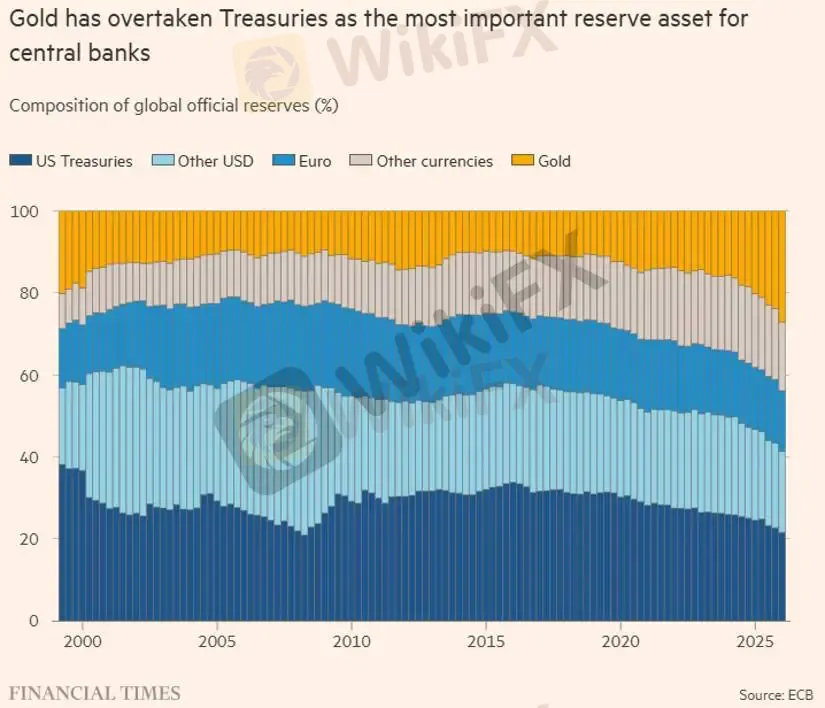

Gold Overtakes TreasuriesSource: ECB, Financial Times

Gold's share of global reserves has risen sharply since 2022, while allocations to U.S. Treasuries have steadily declined. By the end of 2025, gold officially became the largest reserve asset held by central banks worldwide.

The ECB estimates that official gold holdings now exceed 36,000 metric tons, approaching levels last seen during the Bretton Woods era. This reflects a significant shift in reserve management strategies across major economies.

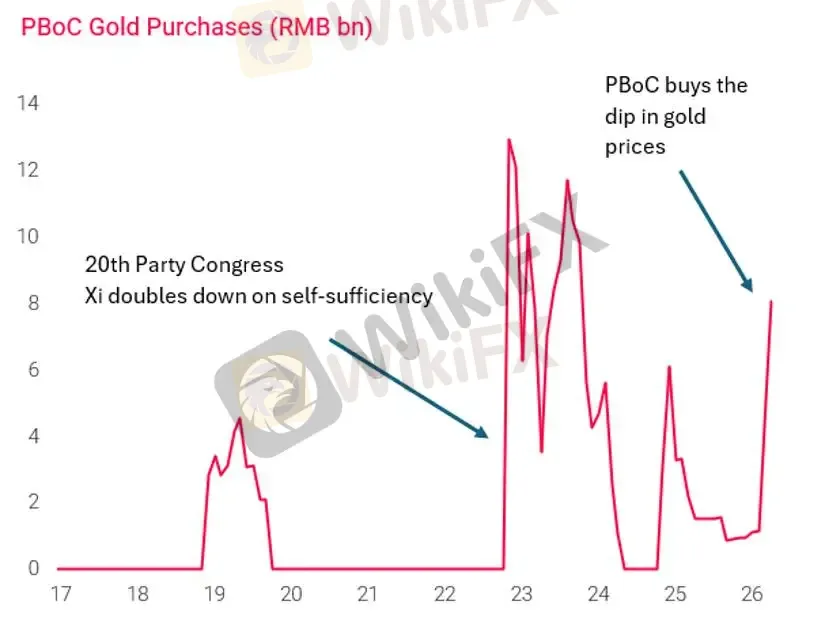

Who Is Buying Gold?Source: TS Lombard

The ECB identifies China, Poland, Turkey, and India as key contributors to recent gold purchases. China's central bank has resumed buying gold and has notably increased purchases during price pullbacks rather than during rallies.

This behavior suggests that central bank demand is driven by long-term strategic allocation rather than short-term market sentiment. Since the freezing of Russia's foreign reserves in 2022, many countries have reassessed reserve security, making physical gold increasingly attractive as a politically neutral asset.

Gold vs. the DollarIt is important to note that gold has surpassed U.S. Treasuries, not the U.S. dollar itself.

According to the ECB, total dollar-denominated assets, including Treasuries, deposits, and other instruments, still account for approximately 42% of global reserves, maintaining the dollar's position as the world's dominant reserve currency.

The current trend represents a gradual diversification within the dollar-based financial system rather than a replacement of the dollar.

What It Means for GoldGold traded near $4,493 on June 2, up 4.2% year-to-date. While the annual gain appears moderate, the underlying demand structure remains highly supportive.

Unlike previous cycles driven by retail investors, today's demand is increasingly supported by central banks, which continue to expand their gold holdings. This creates a stronger and more durable foundation for long-term prices.

Short-term movements will still be influenced by Federal Reserve policy, geopolitical developments, and U.S. dollar fluctuations. However, the ECB report reinforces the view that central bank diversification remains a powerful structural driver for gold.

Key June Catalysts- The $4,400-$4,500 range remains an important accumulation zone for central banks.

- Structural demand from reserve diversification continues to provide support.

- Long-term investors may focus on strategic positioning rather than short-term volatility.

- Currently trading near $74, up 5.6% year-to-date.

- Silver offers higher beta exposure within the precious metals sector and may benefit alongside gold.

The views, analysis, research, prices, and other information presented above are provided for general market commentary only and do not constitute investment advice or represent the official position of this platform. Investors should conduct their own research and carefully assess all risks before making investment decisions.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

BONUS Review 2025: Is This Forex Broker Safe?

WikiFX

WikiFXTrading.com Secures MiCA Licence in Cyprus as Crypto Access Becomes Part of Its EU Strategy

WikiFXThe Hidden Risks of Margin Calls and How to Trade Trends Safely

WikiFXT4Trade Review 2026: Official Warnings and Withdrawal Risks

WikiFXLONG ASIA Review 2026: Withdrawal Complaints and Unverified Regulation

WikiFXTotalFX Dangles 1:1000 Leverage and a $0 Minimum Deposit - But Is Its Regulation Strong?

WikiFXPay a 17% Tax First, Then You Can Withdraw" — How Nixse Allegedly Held One Trader's €25,000 Hostage

WikiFXHow to Read Market Reversals Through Price Action and Indicators

WikiFXA Single TikTok Ad Cost Him RM100,000

WikiFXLONG ASIA Review: Broker Complaints, Regulation Gaps, and Withdrawal Alarms

WikiFXCurrency Calculator

USD

CNY

Current Rate:0

Enter amount

USD

Redeemable Amount

CNY

Calculate